REI vs. 401k

We did a deep dive to compare as closely as possible investing your hard earned money into your 401K against saving for a down payment and acquiring a rental property.

The findings are exciting and motivating! Enjoy the video below.

20 Years later

Today is August 8th 2025. 20 years ago on August 8, 2005 I embarked on owning my first property as a 23 year old single college grad with little experience beyond my credit analyst internship turned PT gig while in college and a few months under my belt working as a mortgage loan officer. Little did I know at the time how valuable it was to have a general understanding on how credit and leverage worked and more importantly having a thorough understanding of the mortgage process and how to qualify would be. Having the understanding of the numbers combined with a clear budget in mind & plan to execute gave me the confidence to move forward and not stress. I will admit this was 3 years before the financial crisis of 08’ and thus I was able to qualify for a mortgage despite having roughly 6 months of a stable job history and less than $3K in my name for funds to close. In fact I financed the down payment funds (2bed 1 bath condo in OOB, ME) via a cash advance on my credit card (which I was able to get the 3% transaction fee waived as I learned a thing or 2 while at MBNA America). I had a 15K credit limit and I did a $12K “cash advance” at 0% for 1 year to have enough money for the down payment, closing costs, as well as furniture for my first place.

That explains how I got to the closing table successfully and below I will breakdown what has become of my this property in which I still own today (8/8/25). I want to highlight that I had very little (NONE) big ticket repair items and that was planned. In 2017 I did replace all the floors in the unit (I believe in high quality & long lasting) which is accounted for in my maintenance cost, as it has averaged out to just under 3% of annual rents collected. Aside from my primary residence I only purchase condo’s and townhomes in which I can leverage HOA’s to the investor advantage. HOA dues are offset by fully eliminating costs associated with new roofs, windows, siding, grading, septic tanks, main water lines, lawn maintenance, tree issues, porches/decks, etc. (aka BIG ticket items). Additionally, my monthly HOA also absorbs 75% of the annual cost of homeowner insurance premiums. The subject property in this article cost $294 annual to insure. The average cost for insurance on a single family home is $1,600 (more than 500% my cost) because a condominium complex has a master insurance policy in place that covers the common areas, interior structures of units, exterior walls, roof, windows, foundation as well as outdoor spaces such as the parking lot, sidewalk and landscaped spaces. Lastly, the HOA “Rules” enable me to leverage them so I’m not the bad guy in the discussion. Let’s be honest what investor wants people smoking in their units (there is a no smoking rule for the entire complex for this particular property) or have loud parties late at night (noise ordinance starts at 10PM) or trash piled out anywhere other than the trash bin (there is a fine if trash is left outside door or anywhere other than the onsite dumpster) to name just a few.

I lived in this property from August 2005 until November 2007. During this time I had a roommate and my total living costs was around $200 per month. The purchase price was $115,000 at a rate of 5.875% 30 yr fix, 5% down ($5,750, if you adjust for inflation that’s equivalent to $9,100 in today’s dollars) bringing my P&I to $646 per month (it’s so nice to have the largest cost be FIXED), taxes were $68 per month, insurance was $19 per month and the HOA was $85 per month. Total monthly costs came to $818 per month and I had a roommate paying me $600 per month. For a near broke 23 year old this was great.

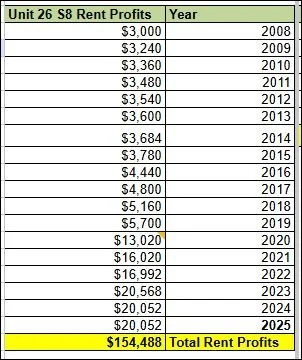

Below is a breakdown of profits I made each year on this property. I want to highlight that I factor for a 3% (of total annual rent collected) maintenance cost in my profits which I deduct from the total number. I derived at this number by tracking my maintenance costs for this exact property type for now 20 years (I currently own 9 condos and 2 townhomes). Additionally, I want to highlight that the town of OOB was rezoned at the end of 2019 and the rent rates became the same of Cumberland county (Portland) rather than York county, thus increasing my rent by 40%. Additionally, I paid off this unit June of 2020 when I did a cash-out refi on another investment unit as I was able to get a 3.25% 30 year fix on a different unit. An added takeaway here is leverage is awesome, especially 30 year fix rate leverage (and if rates drop you can refi) but if rates soar you keep it and stay happy. Essentially the 30 year fix mortgage is a 1 way bet that the investor essentially always wins.

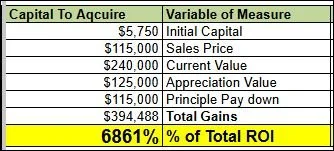

The 2 tables above illustrate how valuable this 1 property has become. A 6861% percent (total yield) return on my initial $5,750. This combines the unrealized (appreciation, 125K + principle paydown, 115K) and realized (rent profits, 154K) adding up to $394,000 in total profits. Take the $394K and divide that by $5,750 to find the total rate of return of 6861%. To help put this in perspective if you purchased $5,750 worth of Salesforce (CRM) stock in August 2005 it would have been $7.94 per share. Today it’s approximately $250 per share. See the data table below. This would amount to a total return of 3057%, which is very strong but only half the return of this property. I did find a stock (Amazon) that produced a 9700% return over this timeframe but the point is, I wasn’t trying to pick the next Amazon but instead a modest investment that would provide me some cashflow and instead it became an extraordinary ROI even with a conservative approach, with patience we nearly all have access to. This is 1 property that had/has very little risk and now pays me a giant monthly dividend with lots of tax advantages which stocks do not have.

📊 Investment Performance (2005–2025) using $5,750 upfront capital to purchase each investment type on August 8, 2005 and what the value is on August 8, 2025.

🔍 Insights:

Amazon outperformed both the property and Salesforce stock, delivering nearly 10,000% return.

My property investment still yielded an exceptional return, more than double Salesforce’s performance.

Salesforce, while strong, lagged behind the other two in terms of total ROI.

🏁 Conclusion: The Power of Patience in Real Estate Investing

Over the past two decades, my modest initial investment of $5,750 in real estate has grown into nearly $400,000 in total gains—a testament to the compounding power of time, equity, and appreciation. While high-performing stocks like Amazon and Salesforce have also delivered impressive returns, real estate offers a unique blend of tangible value, leverage, and stability that can rival even the most dynamic equities.

Long-term real estate investing isn’t just about chasing appreciation—it's about building wealth through consistent equity growth, passive income, and strategic asset management. Whether you're a seasoned investor or just starting out, the key takeaway is clear: time in the market beats timing the market, and real estate remains one of the most reliable vehicles for long-term financial growth.

9 Year Look Back

It all begins with an idea.

April 2025. I’m in the standard process of increasing my rents for each of my rental units as I do every year. In the private market this was always a painful discussion with the tenant who would be frustrated and often ask about doing upgrades to the unit because I’d be increasing the rent by $50 per month so I should be putting a new kitchen in…My annual increases are much different now that I’m currently only renting to Housing Choice Voucher holders. With 11 properties I’m typically increasing a property every other month, some months I have multiple. Increasing a HCV holders rent is based on the HAP contract month and not based on the calendar year. I was reviewing my most recent rent increase today, March 27, 2025 and thought about how at this time 9 years ago I was under contract on this property waiting to close and preparing to get it ready for a housing quality inspection as I knew I would be renting to a HCV holder. This lead me to think about all the numbers I looked at as I led up to making my offer. It was a buyers market in 2016 around the country even in Raleigh North Carolina. Let’s take a close look at how strong of deal this 1 property really was. I’ll do another by the numbers break down in the coming months on 1 of my units in Maine so we can compare geographies and markets.

Official Purchase & Sales signed agreement for 17XX Quail Ridge town home. Closed April, 18th 2016. Purchase price was $105K minus $2,100 from seller concessions bringing my total cost to $102,900.

Excerpt from the P&S on seller concessions:

Debt Service breakdown:

20%

4.5% 30 year fixed conventional loan through BB&T

Total Capital needed $24,000 ($21K down payment plus $5K in CC, minus the $2,100 in seller concessions).

Taxes were $83 per month, Insurance was $38 per month, HOA was $225 per mo.

P&I was and still is $426 per mo.

The total monthly cost was $811 and total rents collected were $1,330 providing a monthly profit of $519. Which at the time was a 25.82% CoC, accounting for the average annual maintenance expenses of 3% of rents. The total yield (cashflow profit, principal paydown, appreciation at 2%) on this property at time of purchase was 40.16% year 1 and by year 10 (2026) annual yield was forecasted at 53% per year.

First HCV Holder tenant moved in on May 1st, 2016 at an approved FMR of $1,330 (she pays utilities).

The current state of this property now in 2025:

My latest rent increase was just approved and goes into effect on June 1st, 2025. I will use this rent rate in breaking down the numbers below.

By the numbers breakdown for this particular property:

Note: Debt service has remained constant as I did not refi.

P&I: $426

Taxes: $197

HOA: $327

Insurance: $81

Total monthly cost: $1,032

My total monthly cost has increased by $260 per month. However, my monthly rents collected has increased by $1,496. Bringing my current total monthly profit to $1,794 (2,826 – 1,032).

As the current numbers sit, here is what this deal is producing accounting for a 3% of monthly rents for maintenance:

I’m just approaching YEAR 9 of ownership. The estimated 53% annual total yield for this property has been clearly achieved by nearly 2 times the expected number as it’s producing in year 9 a total yield of 99.53% (unrealized plus realized gains). However, it’s actually doing WAY better than this because I estimate a conservative 2% annual appreciation which over the course of 9 years would equate to a total appreciation of $20,484. However, the appreciation has exploded in this particular area and I can illustrate below the new value is actually $285,600. This is a total appreciation of $180,600. That’s approximately 11.5% annual appreciation. Which equates to a total annual yield of 139% this year (year 9)

The table below is a side by side comparison of the numbers the first year I purchased this property compared to what I forecasted for the year of 2025 compared to the actual 2025 numbers assuming the new rent rate for the entire year: